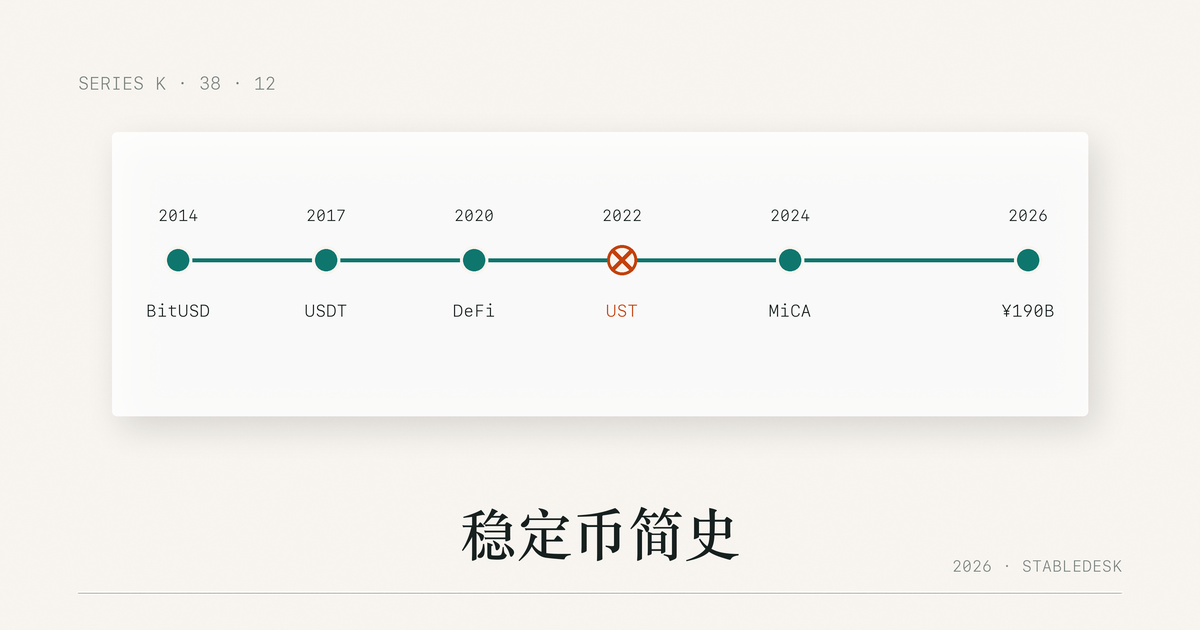

The four eras

It is useful to divide the twelve years into four eras. The first (2014-2017) is the prototype era — Tether emerges, MakerDAO is built, the category exists but is tiny. The second (2018-2020) is the consolidation era — USDT and USDC become the dominant pair, exchanges adopt them as quote assets, the first major depeg happens. The third (2021-2022) is the boom-and-bust — DeFi summer, algorithmic experimentation, Luna's collapse. The fourth (2023-2026) is the regulatory era — SVB / Circle, BUSD wind-down, MiCA, HKMA, the first regulated frameworks at scale.

| Year-end | Total USD-stablecoin supply | USDT share | USDC share | Other tokens (DAI, BUSD, etc) |

|---|---|---|---|---|

| 2017 | ~1.4B | ~95% | — | ~5% |

| 2018 | ~2.3B | ~85% | ~10% | ~5% |

| 2019 | ~5.2B | ~75% | ~10% | ~15% |

| 2020 | ~25B | ~80% | ~12% | ~8% |

| 2021 | ~140B | ~55% | ~30% | ~15% |

| 2022 | ~135B | ~50% | ~33% | ~17% |

| 2023 | ~135B | ~67% | ~17% | ~16% |

| 2024 | ~205B | ~70% | ~22% | ~8% |

| 2025 | ~245B | ~70% | ~24% | ~6% |

| 2026 (mid) | ~270B | ~62% | ~23% | ~15% |

The supply trajectory is striking. From under 1.5 billion at the end of 2017 to a quarter-trillion by mid-2026 — a 200-fold expansion in nine years. Three growth phases stand out: 2019-2020 (DeFi summer triggered the first real adoption wave), 2021 (the bull-market peak doubled supply in twelve months), and 2024-2025 (post-MiCA institutional adoption). The 2022 contraction is visible but more modest than the public reaction suggested.

Era 1 · The prototype years (2014-2017)

Era 2 · The consolidation years (2018-2020)

Era 3 · Boom and bust (2021-2022)

Era 4 · The regulatory years (2023-2026)

The headline lesson from twelve years

Five sub-arcs that ran in parallel

The fiat-backed convergence

Every successful stablecoin at scale has converged on the same reserve composition: short-dated US Treasury bills plus cash at regulated banks plus overnight repos. The "fully reserved by US dollars" claim that was contested in 2018-2021 has become operationally near-universal. The differences across issuers are now matters of degree (which banks, which auditor, which jurisdiction) rather than of category.

The algorithmic disappearance

BitUSD, NuBits, Basis Cash, Empty Set Dollar, Iron Finance, Mim and dozens of smaller projects all attempted some version of algorithmic stabilisation. None have survived at scale as a primary product. UST's collapse in May 2022 marked the practical end of the experiment. MakerDAO's DAI, the one survivor, did so by progressively becoming more fiat-backed (via USDC collateral) rather than more algorithmic. The lesson — algorithmic stablecoins that use a sister token as the absorption mechanism are solvent only when the sister token has more market cap than the stablecoin — is now sector consensus.

The cross-chain expansion

USDT in 2014 was a single-chain product (Bitcoin / Omni). By 2026 USDT exists on Ethereum, Tron, Solana, Avalanche, BSC, Polygon, Arbitrum, Optimism, Aptos, Sui, Ton, Near and a dozen smaller chains, with bridges and native deployments across most. The same pattern holds for USDC. The cross-chain expansion has produced its own risk class (bridge exploits, chain-specific deployments with different security profiles) but has also made stablecoins meaningfully more useful as a payment rail.

The supervisory build-out

In 2014 there was no specific regulatory regime for stablecoins anywhere in the world. By 2026 there are dedicated frameworks in the EU (MiCA), Hong Kong (HKMA stablecoin ordinance), Singapore (MAS guidelines), Japan, the UK (in development), and a fragmented but functional US regime (NY DFS trust framework, federal money-transmitter licensing). The build-out has been faster than most observers expected in 2017-2018 and has produced supervisory clarity that the early years lacked.

The use-case diversification

Stablecoins began as exchange settlement assets. They are now used for cross-border remittance (Tron USDT in Southeast Asia and Latin America), corporate treasury (USDC for crypto-native firms), commerce payments (PYUSD, USDC on Stripe), DeFi collateral (USDC and DAI), short-term yield (USDC, USDT, FDUSD in money-market-style products), and as functional dollar substitutes in jurisdictions with currency restrictions (multiple tokens, deeply distributed). The breadth of use-case is the single largest difference between the 2017 sector and the 2026 sector.

What the next twelve years probably look like

Three plausible trajectories, in rough order of likelihood:

Continued infrastructure deepening. Supply continues to grow to roughly half a trillion by 2030; the share between USDT and USDC stabilises at roughly 60/30; new use cases (small-merchant payments, B2B treasury, programmatic agent-to-agent transfers) emerge incrementally. The sector remains a wholesale infrastructure layer, not a consumer-facing brand category.

Central bank digital currency interaction. Wholesale CBDCs (already piloted by ECB, MAS, BIS) become live in 2027-2028. The CBDCs interact with private stablecoins through clearly defined interface layers. Private stablecoins continue to serve the retail and corporate use cases; CBDCs serve the wholesale settlement use case. The two coexist rather than compete.

A consolidation event. A material adverse event affecting one of the major issuers (a custodian failure, a sustained reserve dispute, a regulator action of unprecedented scale) produces an industry consolidation. Supply migrates toward two or three winners. The sector shrinks in name but not in total value. This is the lower-probability outcome but is non-trivial.

What we do not expect: the disappearance of fiat-backed stablecoins, the success of a new generation of algorithmic models, or the replacement of the dollar-denominated dominant share with a currency basket. The pattern has stabilised enough that radical breaks are unlikely in the next several years.

If you want to act on this

The narrow action is to understand which era's lessons apply to your current holdings. Era 1's lesson is that prototypes are fragile; do not hold significant value in any stablecoin under 12 months old. Era 2's lesson is that consolidation favours the deepest pools; the top two tokens are structurally advantaged. Era 3's lesson is that contagion is real but bounded; diversification across issuers absorbs most of the shock. Era 4's lesson is that supervisory framework matters; preference issuers in clearer regulatory regimes. The desk uses Binance for spot trading; the Binance referral link uses code BN16188; registering does not change your fees.

Twelve-year reference shelf

- CoinGecko and DeFiLlama historical supply data for USDT, USDC, BUSD, DAI, UST, EURC, FDUSD, PYUSD, 2014 through current.

- Tether and Bitfinex disclosures including the Whitepaper (2014), NYAG settlement (2021), CFTC settlement (2021), quarterly attestations from 2021-present (earlier monthly attestations 2017-2020).

- Circle press releases and SEC filings: USDC launch (September 2018), Centre Consortium dissolution (2023), Circle IPO S-1 and subsequent 10-Q filings (2024 onward).

- MakerDAO whitepapers v1 (2014-2015), Single Collateral DAI launch (November 2017), Multi-Collateral DAI launch (November 2019).

- Paxos / Binance BUSD launch announcements (September 2019), NYDFS Consumer Alert (February 2023), Paxos redemption notice (January 2024).

- Terraform Labs disclosures, Anchor Protocol documentation, LFG public statements May 2022; Chainalysis and Nansen analyses of Terra collapse.

- Regulation (EU) 2023/1114 (MiCA), HKMA Stablecoin Issuer Licensing Ordinance (2024), MAS Stablecoin Guidelines (2023), NYDFS guidance series (2018-2024).

- Coinbase, Kraken, Binance, OKX historical ticker data for major depeg events.

- FDIC and Treasury joint statement on SVB (March 12, 2023); Bank Term Funding Programme terms (March 2023-March 2024).

Corrections, additions, or alternative readings of any event in the timeline are welcome. Write to privacy@vsccex.com; the corrections log is on the corrections page.